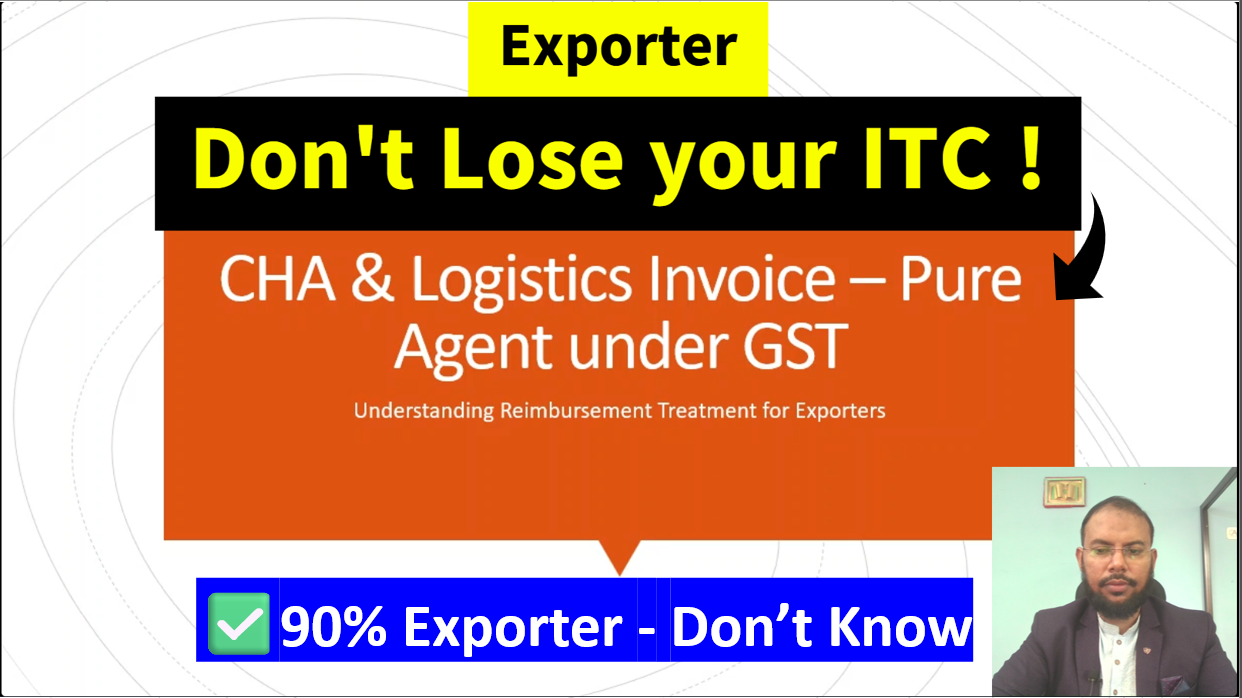

Understanding CHA & Pure Agent Invoicing Under GST for Exporters

"Pure Agent" under Rule 33 of the CGST Rules

GST UPDATES

CA M.F.Khan

7/11/20252 min read

📢 Understanding CHA & Pure Agent Invoicing Under GST for Exporters

In the logistics and export sector, Custom House Agents (CHA) often incur costs on behalf of exporters, such as customs duty, freight, and terminal handling. But how should these expenses be treated under GST? Can a CHA avoid charging GST on these reimbursements? The answer lies in understanding the concept of a "Pure Agent" under Rule 33 of the CGST Rules.

In this article, we'll break down how CHAs can structure their invoices correctly, maintain compliance, and avoid unnecessary GST liabilities.

What is a Pure Agent under GST?

As per Rule 33 of the CGST Rules, a CHA can act as a Pure Agent if they meet all the following conditions:

🔹 Contractual Agreement: There must be a clear agreement with the client (exporter) that the CHA will incur certain expenses as a pure agent.

🔹 No Ownership: The CHA should not hold any title to the goods or services being procured.

🔹 No Personal Use: The services or goods paid for must not be used for the CHA’s own interest.

🔹 Exact Reimbursement: Only the actual amount paid should be recovered—no markup allowed.

CHA Invoice Sample: Taxable vs Pure Agent Components

Here is an example of a sample CHA invoice with both taxable services and pure agent reimbursements:

DescriptionAmount (INR)Taxable?CHA Service Fee₹10,000✅ Yes (18% GST)Documentation Charges₹1,500✅ Yes (18% GST)Freight Charges₹23,600❌ No (Pure Agent)Terminal Handling Charges₹3,000❌ No (Pure Agent)Customs Duty₹5,000❌ No (Pure Agent)

📊 Invoice Summary:

Taxable Value: ₹11,500

GST @ 18%: ₹2,070

Reimbursements (Pure Agent/Non-Taxable): ₹31,600

Total Invoice Value: ₹45,170

This example clearly separates taxable charges from pure agent reimbursements, ensuring compliance and avoiding overcharging GST.

Compliance Checklist for CHA Acting as Pure Agent

To safely treat expenses as non-taxable under the Pure Agent concept, CHAs must ensure the following:

✅ Tripartite Agreement: There must be a clear agreement between the CHA and exporter for acting as a pure agent.

✅ Invoices in Exporter's Name: All third-party services (freight, duty, etc.) must be billed directly to the exporter.

✅ No Markup: Pure Agent reimbursements must be exact; any markup invalidates the exemption.

✅ Proper Invoice Disclosure: CHA invoices must clearly mention the split between taxable services and reimbursements.

✅ Supporting Documents: Attach proofs like freight invoices, duty challans, and terminal receipts.

❗ What If Pure Agent Conditions Are Not Met?

If even one of the Pure Agent conditions is not fulfilled:

⚠️ The entire invoice becomes taxable under GST, including all reimbursements.

This could lead to an 18% tax on the full value, increasing costs unnecessarily and causing compliance issues.

Final Thoughts

Acting as a Pure Agent under GST allows CHAs to legitimately exclude third-party costs from GST liability—but only if all the conditions are strictly met. For exporters, this ensures transparency, reduced tax burden, and better documentation.

For professional assistance with your CHA invoicing and GST filing, feel free to contact our team at CAMF Khan & Associates — we’re here to simplify your compliance journey.

Are you an exporter? Beware! 90% exporters lose their GST ITC due to common mistakes in GSTR 2B, ITC claim, and Pure Agent compliance. Understand the right export business practices, GST filing tips, and ITC reconciliation techniques. Learn about Pure Agent under GST, refund claim procedures, GSTR-1 filing, GSTR-2B reconciliation, GST ITC revision, and the correct Pure Agent Invoice Format. This video is your one-stop guide if you're searching for: export, exporter, gst, gst itc claim, pure agent in gst, idt ca final, ca near me, @ca.mfkhan, gst update, gst itc 04 filing, and more. Don’t risk your refund—know the law, claim it right!